By Nikolaos Bourtzis.

Monetary policy has become the first line of defense against economic slowdowns — it’s especially taken the driver’s seat in combating the crisis that began in 2007. Headlines everywhere comment on central bank’s (CB) decision-making processes and reinforce the idea that central bankers are non-political economic experts that we can rely on during downturns. They rarely address, however, that central banks’ monetary policies have failed repeatedly and continue to operate on flawed logic. This piece reviews recent monetary policy efforts and explains why central bank operations deserve our skepticism–not our blind faith.

What central banks try to do

To set monetary policy central banks usually target the interbank rate, the interest rate at which commercial banks borrow (or lend) reserves from one another. They do this by managing the level of reserves in the banking system to keep the interbank rate close to the target. By targeting how cheaply banks can borrow reserves, the central bank tries to persuade lending institutions to follow and adjust their interest rates, too. In times of economic struggle, the central bank attempts to push rates down, such that lending (and investing) becomes cheaper to do.

This operation is based on the theory that lower interest rates discourage savings and promote investment, even during a downturn. That’s the old “loanable funds” story. According to the neoclassical economists in charge at most central banks, due to rigidities in the short run, interest rates sometimes fail to respond to exogenous shocks. For example, if the private sector suddenly decides to save more, interest rates might not fall in response. This produces mismatches between savings and investment; too much saving and too little investment. As a result, unemployment arises since aggregate demand is lower than aggregate supply. In the long run, though, these mismatches will disappear and the loanable funds market will clear at the “natural” interest rate which guarantees full employment and a stable price level. But to speed things up, the CB tries to bring the market rate of interest towards that “natural” rate through its interventions.

Recent Attempts in Monetary Policy

However, interest rate cuts miserably failed to kick-start the recovery during the Great Recession. That prompted the use of unconventional tools. First came Quantitative Easing (QE). Under this policy, central banks buy long-term government bonds and/or other financial instruments (such as corporate bonds) from banks, financial institutions, and investors, which floods banks with reserves to lend out and financial markets with cash. The cash is then expected to eventually filter down to the real economy. But this did not work either. The US (the first country to implement QE in response to the Crash) is experiencing its longest and weakest recovery in years. And Japan has been stagnating for almost two decades, even though it started QE in the early 2000s.

Second came “the ‘natural rate’ is in negative territory” argument; Larry Summers’ secular stagnation hypothesis. The logic is that if QE is unable to increase inflation enough, negative nominal rates have to be imposed so real rates can drop to negative territory. Since markets cannot do that on their own, central banks will have to do the job. First came Sweden and Denmark, then Switzerland and the Eurozone, and last but not least, Japan.

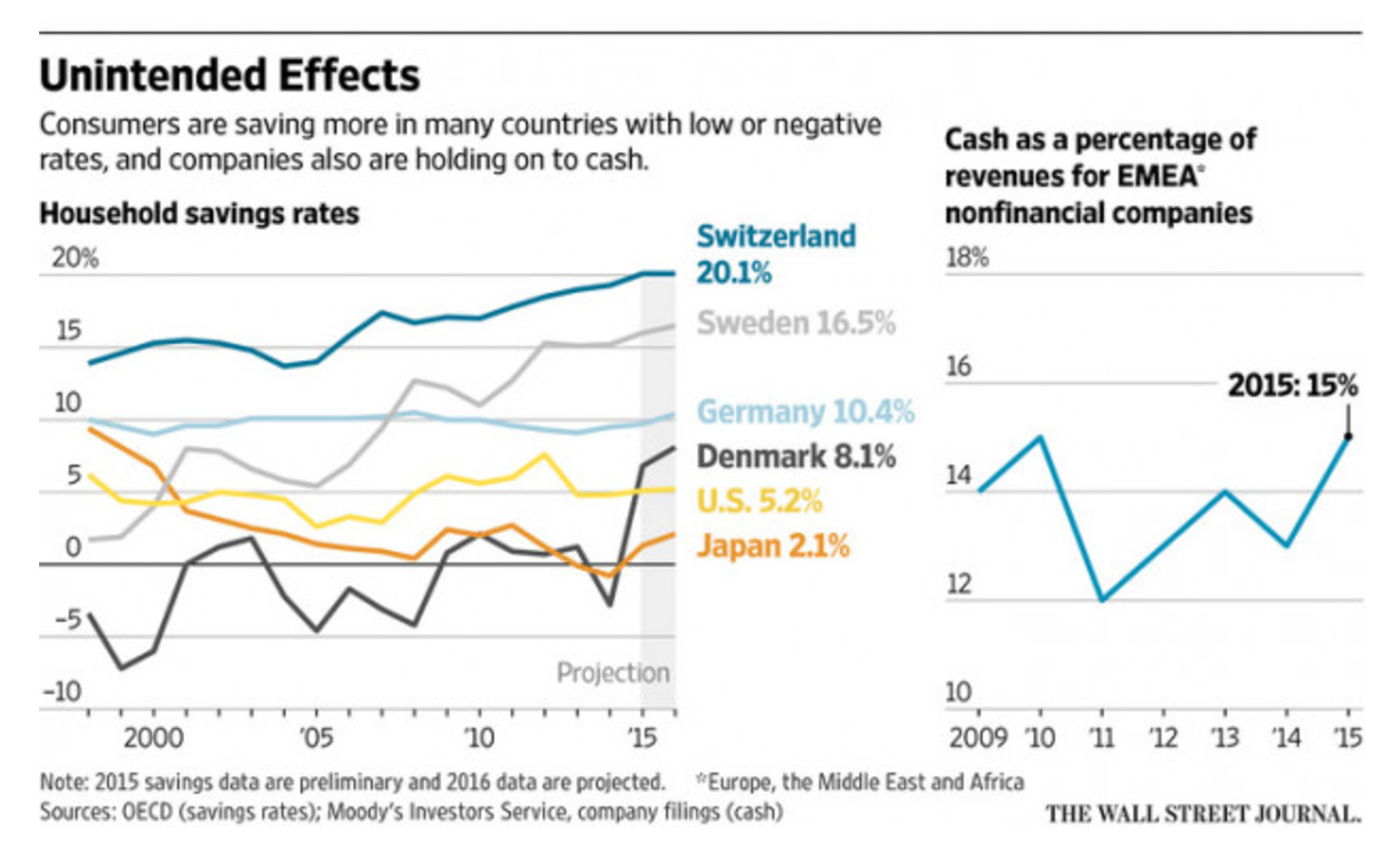

Not surprisingly, the policy had the opposite effect of what was intended. Savings rates went up, instead of down, and businesses did not start borrowing more; they actually hoarded more cash. Some savers are taking their money out of bank accounts to put them in safe deposits or under their mattresses! The graph below shows how savings rate went up in countries that implemented negative rates, with companies also following suit by holding more cash.

Central bankers seem to be doing the same thing over and over again, while expecting a different outcome. That’s the definition of insanity! Of course, they cannot admit they failed. That would most definitely bring chaos to financial markets, which are addicted to monetary easing. Almost every time central bankers providea weaker response than expected, the stock market falls.

There is too much private debt.

So how did we get here? To understand why monetary policy has failed to lift economies out of crises, we have to talk about private debt.

Private debt levels are sky high in almost every developed country. As more and more debt is piled up, it becomes more costly to service it. Interest payments start taking up more and more out of disposable income, hurting consumption. Moreover, you cannot convince consumers and businesses to borrow money if they are up to their eyeballs in debt, even if rates are essentially zero. What’s more, some banks are drowning in non-performing loans so why would they lend out more money, if there is no one creditworthy enough to borrow? Even if private debt levels were not sky high, firms only borrow if capacity needs to expand. During recessions, low consumer spending means low capacity utilization, so investing in more capacity does not make sense for firms.

How to move forward

So, now what? Should we abolish central banks? God no! Central banks do play an important role. They are needed as a lender of last resort for banks and the government. But they should not try to fight the business cycle. Tinkering with interest rates and buying up financial instruments encourages speculation and accumulation of debt, which further increases the likelihood of financial crises. The recent pick-up in economic activity is again driven by private debt and even the Bank of England is worried that this is unsustainable and might be the trigger of the next financial crisis.

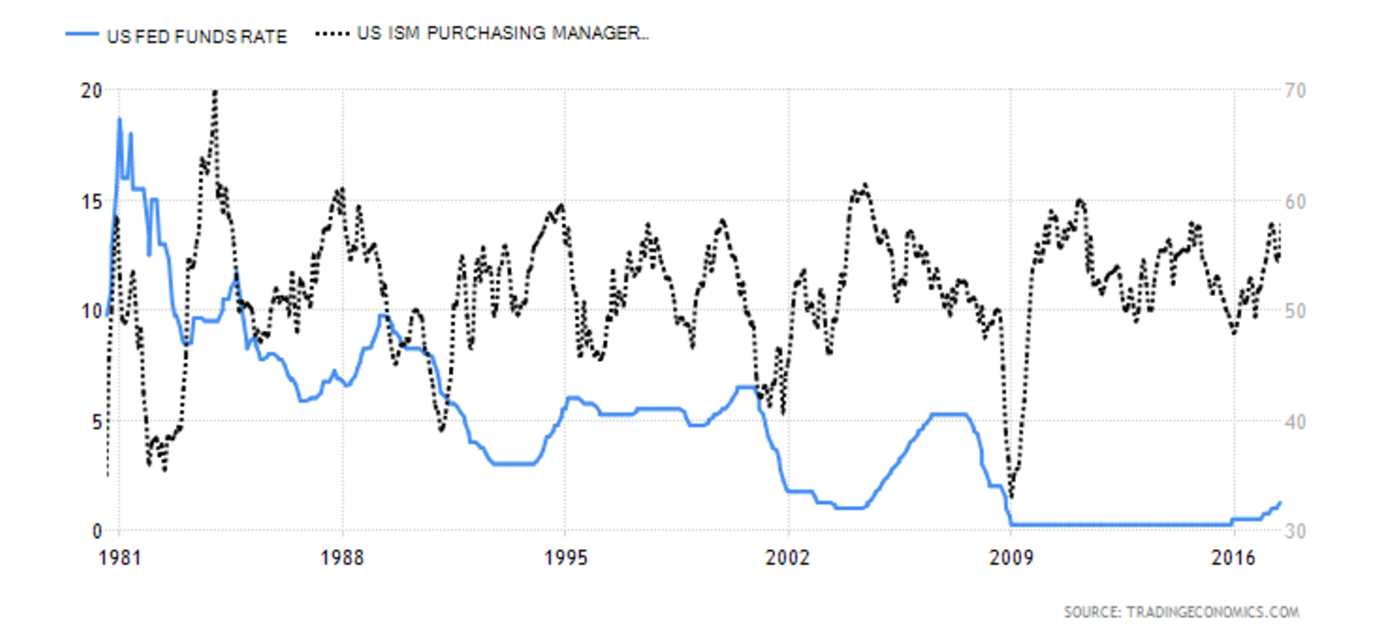

The success of monetary policy depends on market mechanisms. Since this is an unreliable channel that promotes economic activity through excessive private debt growth, governments should be in charge of dealing with the business cycle. The government is the only institution that can pump money into the economy effectively to boost demand when it is needed. But due to the current misguided fears of large deficits, governments have not provided the necessary fiscal response. Investment requires as little uncertainty as possible to take place and only fiscal policy can reduce uncertainty. Admittedly in previous decades, monetary responses might have been responsible for restoring some business confidence as shown in the figure below.

This effect, though, cannot always be relied upon during severe slumps. And no doubt, more attention needs to be given to private debt, which has reached unprecedented levels.

Monetary policy has obviously failed to produce a robust recovery in most countries. It might have even contributed in bringing about the financial crisis of 2008. But central bankers refuse to learn their lesson and keep doing the same thing again and again. They don’t understand that their policies have failed to kick-start our economies because the private sector is drowning in debt. It’s time to put governments back in charge of economic stabilization and let them open their spending spigots. A large fiscal stimulus is needed if our economies are to recover. Even a Debt Jubilee should not be ruled out!

About the Author

Nikos Bourtzis is from Greece, and recently graduated with a Bachelor in Economics from Tilburg University in the Netherlands. He will be pursuing a Master in Economics and Economic analysis at Groningen University. Research interests are heterodox macroeconomics, anti-cyclical policies, income inequality, and financial instability.

Monetary policy is insufficient to properly describe and understand the entire macro-economy in the way that my model does. It is not that my model (in SSRN 2865571) is so cleaver, but that to look at only one side of our social system is to avoid all the aspects of it that are significant but don’t include money. One of these vital aspects is the right of access to sites of land.

Unless we can share the opportunities that useful land provides, all the money associated with it will not help us–in fact it will limit us in what we rightly should be making of the bounty the land gives. The problem of getting a clear understanding about this was compounded when in about 1900 John Bates Clark and others began to politicize the knowledge by making land appear as if it were durable capital goods. This means that apparently one can speculate in it in the same way as holding shares in a company of product makers.

Land has some very different properties which mean that its monopoly is damaging to those for which its access is denied and that includes at least 60% of the present population. Poor people have lost the opportunities that land access once gave. It used to be free, when the commons land in the UK was an established means for poor people to get limited benefit from its use, but with the enclosures acts, commons land was no longer shared and poor people starved because they had no place to raise their very limited farming activities.

However money can be better used to control access rights to land so the best money policy regarding land is to tax land values.

Socially Just Taxation and Its Effects (17 listed)

Consider how land becomes valuable. New settlers in a region begin to specialize and this improves their efficiency in producing specific goods. The central land is the most valuable due to easy availability and least transport needed. This distribution in land values is created by the community and (after an initial start), not by the natural resources. As the city expands, speculators in land values will deliberately hold potentially useful sites out of use, until planning and development have permitted their values to grow. Meanwhile there is fierce competition for access to the most suitable sites for housing, agriculture and manufacturing industries. The limited availability of useful land means that the high rents paid by tenants make their residence more costly and the provision of goods and services more expensive. It also creates unemployment, causing wages to be lowered by the monopolists, who control the big producing organizations, and whose land was already obtained when it was cheap. Consequently this basic structure of our current macroeconomics system, works to limit opportunity and to create poverty, see above reference.

The most basic cause of our continuing poverty is the lack of properly paid work and the reason for this is the lack of opportunity of access to the land on which the work must be done. The useful land is monopolized by a landlord who either holds it out of use (for speculation in its rising value), or charges the tenant heavily for its right of access. In the case when the landlord is also the producer, he/she has a monopolistic control of the land and of the produce too, and can charge more for this access right than what an entrepreneur, who seeks greater opportunity, normally would be able to afford.

A wise and sensible government would recognize that this problem derives from lack of opportunity to work and earn. It can be solved by the use of a tax system which encourages the proper use of land and which stops penalizing everything and everybody else. Such a tax system was proposed 136 years ago by Henry George, a (North) American economist, but somehow most macro-economists seem never to have heard of him, in common with a whole lot of other experts. (I would guess that they don’t want to know, which is worse!) In “Progress and Poverty” 1879, Henry George proposed a single tax on land values without other kinds of tax on produce, services, capital gains etc. This regime of land value tax (LVT) has 17 features which benefit almost everyone in the economy, except for landlords and banks, who/which do nothing productive and find that land dominance has its own reward.

17 Aspects of LVT Affecting Government, Land Owners, Communities and Ethics

Four Aspects for Government:

1. LVT, adds to the national income as do other taxation systems, but it replaces them.

2. The cost of collecting the LVT is less than for all of the production-related taxes–tax avoidance becomes impossible because the sites are visible to all.

3. Consumers pay less for their purchases due to lower production costs (see below). This creates greater satisfaction with the management of national affairs.

4. The national economy stabilizes—it no longer experiences the 18 year business boom/bust cycle, due to periodic speculation in land values (see below).

Six Aspects Affecting Land Owners:

5. LVT is progressive–owners of the most potentially productive sites pay the most tax.

6. The land owner pays his LVT regardless of how his site is used. A large proportion of the ground-rent from tenants becomes the LVT, with the result that land has less sales-value but a significant “rental”-value (even when it is not used).

7. LVT stops speculation in land prices and the withholding of land from proper use is not worthwhile.

8. The introduction of LVT initially reduces the sales price of sites, even though their rental value can still grow over a longer term. As more sites become available, the competition for them is less fierce.

9. With LVT, land owners are unable to pass the tax on to their tenants as rent hikes, due to the reduced competition for access to the additional sites that come into use.

10. With LVT, land prices will initially drop. Speculators in land values will want to foreclose on their mortgages and withdraw their money for reinvestment. Therefore LVT should be introduced gradually, to allow these speculators sufficient time to transfer their money to company-shares etc., and simultaneously to meet the increased demand for produce (see below).

Three Aspects Regarding Communities:

11. With LVT, there is an incentive to use land for production or residence, rather than it being unused.

12. With LVT, greater working opportunities exist due to cheaper land and a greater number of available sites. Consumer goods become cheaper too, because entrepreneurs have less difficulty in starting-up their businesses and because they pay less ground-rent–demand grows, unemployment decreases.

13. Investment money is withdrawn from land and placed in durable capital goods. This means more advances in technology and cheaper goods too.

Four Aspects About Ethics:

14. The collection of taxes from productive effort and commerce is socially unjust. LVT replaces this extortion by gathering the surplus rental income, which comes without any exertion from the land owner or by the banks–LVT is a natural system of national income-gathering.

15. Bribery and corruption on information about land cease. Before, this was due to the leaking of news of municipal plans for housing and industrial development, causing shock-waves in local land prices (and municipal workers’ and lawyers’ bank balances).

16. The improved use of the more central land reduces the environmental damage due to a) unused sites being dumping-grounds, and b) the smaller amount of fossil-fuel use, when traveling between home and workplace.

17. Because the LVT eliminates the advantage that landlords currently hold over our society, LVT provides a greater equality of opportunity to earn a living. Entrepreneurs can operate in a natural way– to provide more jobs. Then earnings will correspond to the value that the labor puts into the product or service. Consequently, after LVT has been properly introduced it will eliminate poverty and improve business ethics.

TAX LAND NOT LABOR; TAX TAKINGS NOT MAKINGS!

So many mistakes in the above article that I don’t know where to start, but here are a few.

1. Interest rate cuts do not depend on the loanable funds theory. I.e. given lower rates, private banks will create and lend out more money than they would at a higher rate.

2. Whence the idea that interest rate cuts “miserably failed” to raise demand? The fact that interest rate cuts did not work as quickly or effectively as we might have wanted does not prove they do not have any effect at all.

3. “As more and more debt is piled up, it becomes more costly to service it.” Er – no. The fall in interest rates has more than compensated for the rise in debts. I.e. the proportion of people’s income that they devote to servicing debt has actually decline.

Ralph Musgrave, your points in turn:

1. as demand for credit rises so banks can charge more. That is, they raise interest rates. If a CB were to reduce rates at a time of high credit demand, unlikely as that is, it becomes less attractive for banks to lend.

2. I have seen no evidence whatever that the post-2008 crash interest rate falls have driven demand for goods and services one jot. Indeed demand fell very sharply and has hardly recovered ten years on. The extra money generated as part of the response was all lost on pushing up the demand for assets.

3. In aggregate your statement may or may not be true but it is irrelevant. The poorer the borrower and the less creditworthy in the view of the banks, the higher the rates of actual interest they pay, both in nominal and real terms. It is there the threat of default is highest. As rates begin to rise those people will find it ever more difficult to service their debts and that is where danger of recession lies.

monetary policy is the process by which the monetary authority of a country controls the supply of money. for this policy inflation problem may arise….