“The tide of Totalitarianism which we have to counter is an international phenomenon and the liberal renaissance which is needed to meet it and of which first signs can be discerned here and there will have little chance of success unless its forces can join and succeed in making the people of all the countries of the Western World aware of what is at stake.” (Friedrich Hayek)

In the past year we’ve seen a number of mentions to the maladies that neoliberalism and globalization have brought upon Western societies (e.g., see here, here, and here). It is well known that during the past decades the levels of inequality and wealth concentration have continued to increase in capitalist economies, leading to the arrival of “outsiders” to the established political powers such as Trump in the US and Macron in France, a turn to the right all over Latin America, and Brexit.

Neoliberalism, one of the main elements to blame, is better known for the policies that defined the world economy since the 1970s. Faithful devotees like Ronald Reagan and Margaret Thatcher, in the US and UK respectively, exported a number of their neoliberal policies to low and middle income countries through the Washington Consensus under the pretense that it would bring about development.

Neoliberal policies did not exactly turn out the way their creators envisioned. They wanted to reformulate the old liberal ideas of the 19th century in a deeper and coherent social philosophy – something that was actually never accomplished. This article will review some of the origins of neoliberalism.

The first time the term “neoliberalism” appeared, according to Horn and Mirowski (2009), was at the Colloque Walter Lippmann in Paris, in 1938. The Colloque was organized to debate the ideas presented in Lippmann’s recent book The Good Society in which he proposed an outline for government intervention in the economy, establishing the boundaries between laissez-faire – a mark of the old liberalism – and state interventionism.

Lippmann set the foundations for a renovation of the liberal philosophy and the Colloque was a first opportunity to discuss the classical liberal ideas and to first draw a line in what the new liberal movement would or should differ from the old liberalism. It was a landmark that, in subsequent years, sparked several attempts to establish institutions that would reshape liberalism, such as the Free Market Study at the University of Chicago and Friedrich Hayek’s Mont Pelerin Society (MPS).

This event announced major difficulties among the peers of liberalism. Reservations and disagreements among free market advocates were not uncommon. A notable mention is Henry Simons, of the Chicago School, whose position against monopolies and how they should be addressed was a point of disagreement with fellow libertarians such as Hayek, Lionel Robbins – both at the London School of Economics (LSE) at the time – and Ludwig von Mises.

Simons’s view that the government should nationalize and dismantle monopolies would nowadays be viewed as a leftist attack on corporations but it fits perfectly under the classical liberal basis that Simons and Frank Knight, also from the University of Chicago, were following. Under their interpretation, any concentration of power that undermines the price system and therefore threatens market – and political, individual – freedoms should be countered, even if it meant using the government for that purpose.

It becomes clear that the reformulation of liberal ideas into what we know today as neoliberalism was not a smooth and certain project. In fact, market advocates struggled to make themselves heard in a world guarded by state interventionism that dominated the Great Depression and post-war period. Keynes’s publication of The General Theory in 1936 and the wake of the Keynesian revolution, swiped economic departments all over and further undermined the libertarian view.

By the end of the 1930s and of Lippmann’s Colloque, however, the perception that neoliberalism would only thrive if there were a concerted collective effort by its representatives changed Hayek’s perception over his engagement in the normative discourse. In 1946-47, the establishment of the Chicago School and the MPS, were both results of a transnational effort to shape public policy and fit liberal ideas under a broader social philosophy. The main protagonists beyond Hayek were Simons, Aaron Director, and the liberal-conservative Harold Luhnow, then director of the William Volker Fund and responsible for devoting funds to the projects.

The condition for success, as remarked in the epigraph, was to “join and succeed in making the people of all the countries of the Western World aware of what is at stake.” What was at stake? Social and political freedom. Hayek and many early neoliberals understood that any social philosophy or praxis crippling market mechanisms would invariably lead to a “slippery slope” towards totalitarianism.

It is important to note, though, that the causation runs from market to social and political freedom and not the other way around. As Burgin (2012) indicates, while market freedom is a precondition to a free democratic society, the latter may threaten market freedom. Free market should not be subjected to popular vote, it should not be ruled over by any “populist” government (a common swear-word today), and there needs to exist mechanisms to protect that from happening.

Once we have that in mind, it is not so bugging the association that Hayek, Milton Friedman, and the Chicago School once had with authoritarian governments such as Pinochet’s in Chile, one of the most violent dictatorships in Latin American history.

Several liberal economists that occupied important public positions in the Chilean dictatorship had been trained at the Chicago School. The famously known “Chicago Boys” first experimented in Chile what later would be applied in the US and UK and then exported to the rest of the developing world through the Washington Consensus.

In brief, the adoption of some form of authoritarian control over popular sovereignty was deemed acceptable in order to guarantee market sovereignty.

Nevertheless, in the discussions within the early neoliberal groups the boundaries of disciplinary economics were trespassed, and the formulation of neoliberalism – and the Chicago School and MPS – was not grounded on any scientific analytical basis but simply on political affiliation.

The multidisciplinary character, dispersion, and incertitude are some of the reasons why it is hard to give a straightforward definition of what the term “neoliberalism” really means. In order to understand it, we have to mind the set of “dualisms” (capitalism vs. socialism; Keynesianism vs. liberalism; freedom vs. collectivism, and so on) that marked the period. Its defenders (academics, entrepreneurs, journalists, etc.) did not know what their own agenda was – they only knew what they were supposed to oppose. Neoliberalism was born out of a “negative” effort.

It wasn’t until many years later that the division between normative and positive economics came to surface with Friedman and his book Capitalism and Freedom, published in 1962. The increasing participation of economists in the MPS, and a more active public policy advocacy by Milton Friedman brought an end to Hayek’s intention to construct a new multidisciplinary social philosophy.

Economically, Friedman embraced laissez-faire; methodologically, he embraced empirical analysis and positive policy recommendations, getting ever further away from abstract notions of value and moral discussions that his earlier MPS fellows, such as Hayek, were worried about. Neoliberalism lost its path on the way to its triumph; it became a “science” that offered legitimacy to a new credo, a new “illusion”.

As the shadows of neoliberalism became more intertwined with the current neoclassical economics and Friedman’s monetarism, it not only lost its name but also gave birth to a corporate type of laissez-faire; one in which social relations are downgraded to market mechanisms; politics, education, health, employment, it all could fit under the market process in which individuals maximize their own utility. There’s nothing that the government can do that the market cannot do better and more efficiently. Monopolies, if anything, are to be blamed on government actions, while labor unions are disruptive to the economy’s wellbeing. Neoliberalism became a set of policies to be followed: privatization, deregulation, trade liberalization, tax cuts, etc. on a crusade to commoditize every single essential service – or every aspect of life itself.

Hayek believed that these ideas could spread and change the world. And they certainly did. What is worth noting is that there is no fatalistic understanding that neoliberalism was unavoidably a result of historical factors.

The rise of neoliberalism was not spontaneous but rather orchestrated and planned; it was a collective transnational movement to counteract the mainstream of the time; it was originated out of delusion in a period marked by wars, authoritarianism and economic crisis; it was grounded on political affiliations and supported by the dominant ruling class that funded its endeavors and transformed public opinion. These are the roots of what is now the mainstream economic thought.

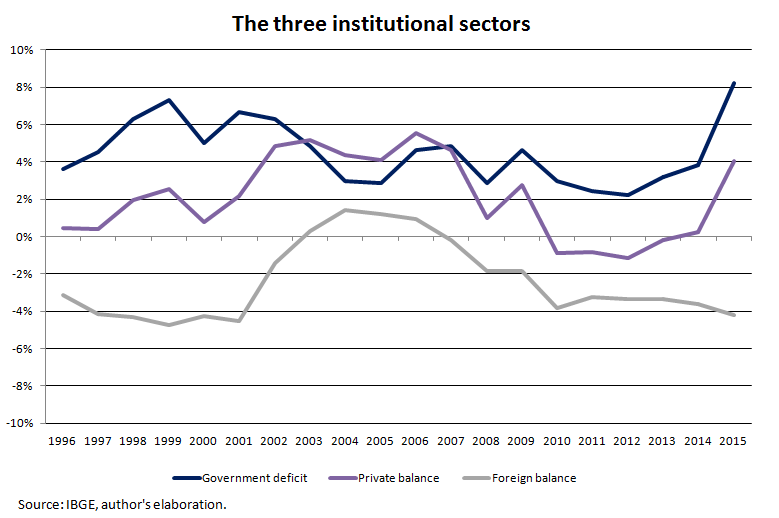

International conditions also played a major role in boosting the domestic economy. High international liquidity and the commodity-price super cycle guaranteed appreciation of the exchange rate, which beyond positively impacting domestic real wages, also helped to keep inflationary pressures under control by making foreign goods more accessible.

International conditions also played a major role in boosting the domestic economy. High international liquidity and the commodity-price super cycle guaranteed appreciation of the exchange rate, which beyond positively impacting domestic real wages, also helped to keep inflationary pressures under control by making foreign goods more accessible.