Whether you’re looking for a job in economics, exploring a new hypothesis, or working to publish your first paper, you might wonder: can you do this in excel? And if not, how much coding should you learn, and how will you learn it? By Kurt Semm

Five years ago, I was studying Romantic literature, and writing my sonnets. Now, I’m a Junior Economist, a Ph.D. Candidate, and comfortable coding in LaTex, Python, R, & Stata. Looking back, there were plenty of pitfalls along the way, and many of them could have been avoided with a little extra guidance.

In an attempt to spare others the struggle, I set out to determine the best rules of thumb in a recent episode of YSI’s Early Career Time.

Pier-André Bouchard St-Amant, a mathematician with a Ph.D. in economics who specializes in the analysis and optimization of public policy reforms and business practices. He teaches quantitative methods and data science at ÉNAP.

Tim Fong, a data scientist whose Silicon Valley experience has ranged from computer vision to net worth data. He has an M.S. in statistics from Baruch College and a JD from the USF School of Law. His economic interest are in post-Keynesian price theory.

Listen to the whole conversation here, or keep reading for their 10 biggest tips.

Don’t be intimidated. Coding just means telling computers what you want them to do. It comes down to making calculations, opening files, opening or closing loops, and creating tables or graphs.

Don’t use excel. Government organizations might do this, but it can lead to a lot of errors. And imagine scrolling over 1,000,000 observations in a single spreadsheet.

Choose one language to start with. Master it, and only then branch out to others. Academic economists tend to prefer Stata because it’s best for running regressions. R is helpful with cleaning Data & makes beautiful plots/graphics (ggplot2). Python is popular in the private sector.

Stay organized. Remember to create a solid file system before you start coding, and make sure to write notes to yourself about what your code is doing. This will help your future self to replicate your work.

Go deep. See if your school, University, or Program teaches a Computer Science Class. These often give you a more in-depth understanding than online certification courses. And the certificates don’t tend to matter that much.

Say bye to Microsoft Word. If you’d like to get published, you’ll need to learn LaTex. It helps create nice-looking summary statistics and saves you a lot of time in the formatting stage of your research.

Expect frustration. There will be times you’ll want to throw your laptop against the wall. Coding is frustrating because errors are inevitable. It never works the first time. Keep at it, and you’ll get through.

Think carefully about your research question first If you want to get through the frustration, you need to care about your research question. Don’t study a question if you don’t care about the answer. Look for something that scares you a bit.

Remember that it’s just a tool Any coding should be in service of your ideas, which are probably nuanced, complex, subjective, and evolving. Don’t reduce your ideas to the level of your coding skills. Improve your code to serve your ideas.

Enjoy the journey. There is a lot to learn, and many resources out there to help you. Here’s a small selection:

About the Author: Kurt Semm is a Junior Economist at the Institute of New Economic Thinking. Simultaneously, he is a Ph.D. Student at the New School for Social Research. He received his BA at St. John’s University in Literature and Economics and an MS from the New School for Social Research. His main areas of research are Ecology, Political Economy, and Water Resources. His research deals with water management and allocation, regional development, and equity, with a particular interest in the Southwest United States.

Thought this was interesting? Keep an eye out for more episodes of YSI’s Early Career Time. Each one explores a challenge in publishing, teaching, the job market, work-life balance, and the various institutional barriers young researchers face. If there’s a topic you’d like us to take up, let us know in the comments below.

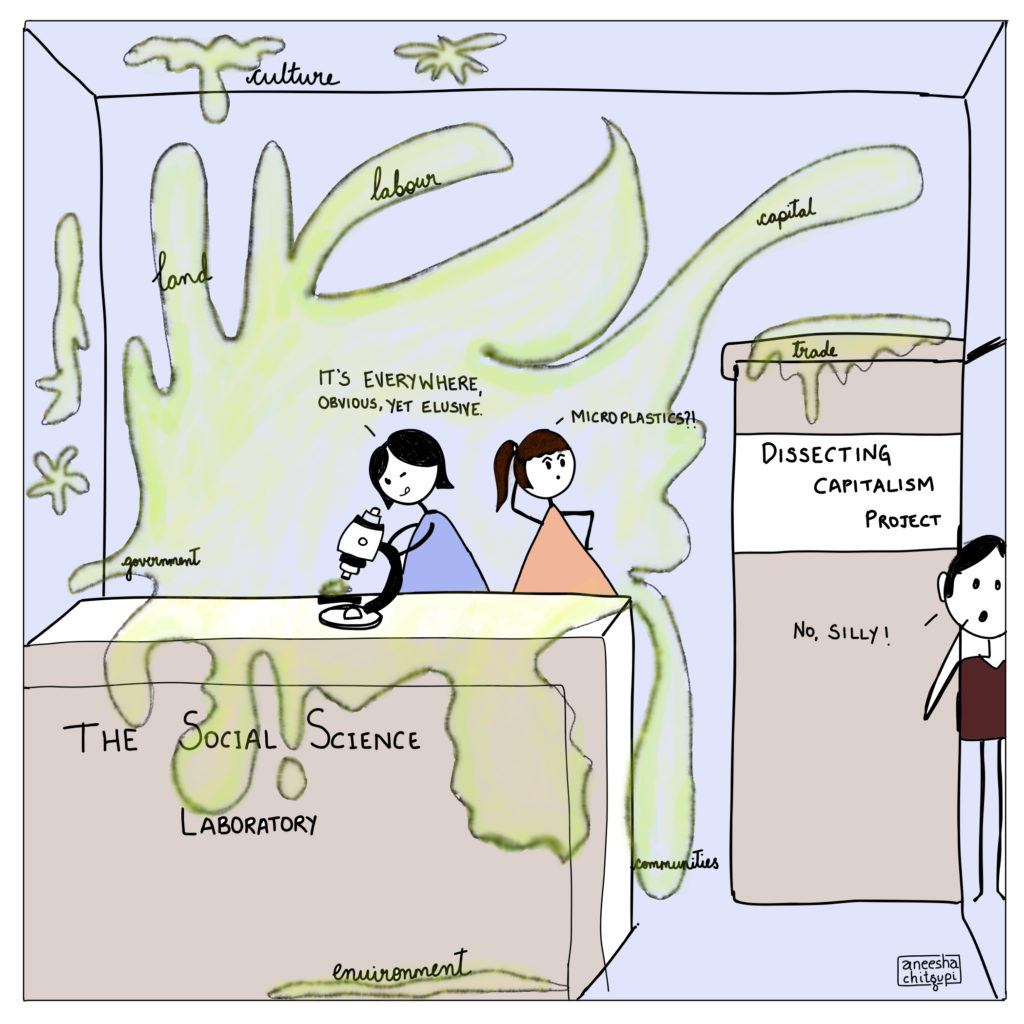

By Shyam Soundararajan | Dissecting Capitalism is a recurring webinar series in the South Asia Working Group that aims to organize a webinar series on the dominant ideology/economic system – capitalism. It aims to explore the tenets of capitalism over the fabric of time and examine its influence on the economy and social classes.

Over the course of 8 webinar sessions in November and December 2021, this project has brought together scholars from various fields of academia such as economics, philosophy, social policy, and law to dissect capitalism through their unique theoretical and empirical lenses. This webinar series was organized by Sattwick Dey Biswas, Aneesha Chitgupi, and Shyam Soundararajan.

Before YSI South Asia hosts Season II of Dissecting Capitalism: Its past, present and future, here is a snapshot of the topics covered under Season I

Illustration by Aneesha Chitgupi

1. Globalization as a Threat to Democracy

The introductory session of the Webinar Series featured Professor Daniel W. Bromley, a Professor of Applied Economics at the University of Wisconsin-Madison. This session was centered on globalization, international trade and democracy and was based on the book, “Possessive Individualism: A Crisis of Capitalism”.

Through this session, Professor Bromley was able to provide an interactive lecture on why globalization is a threat to democratic coherence. Through this lecture, Professor Bromley was able to unveil and demonstrate the hidden reality that globalization weakens the ability of national governments to confront economic crises.

Overall, this session displayed the problems that capitalism has imposed upon national governments, namely the inability to confront economic problems due to the issue of losing “global competitiveness”. View here

2. Multidimensional Poverty around the world: Unmasking Disparities

This session featured Dr. Sabina Alkire, the Director of the Oxford Poverty and Human Development Initiative at the University of Oxford. This session was centered around the Multidimensional Poverty Index (MPI), which measures poverty using a variety of factors.

Through this webinar, Dr. Alkire was able to explain more about the MPI by explaining its methodology. After this, Dr. Alkire presented the findings of the October 2021 global MPI report. In addition to this, Dr. Alkire discussed and dissected various disparities across ethnic groups and populations.

Overall, this webinar presented the impact of capitalism and its various endemic traits on poverty around the world. By discussing the MPI, Dr. Alkire was able to demonstrate how capitalism actively contributes to major poverty trends around the world. View here

3. Compressed Capitalism and Late Development in India

This session featured Professor Dr. Anthony P. D’Costa, an Eminent Scholar in Global Studies and Professor of Economics at the University of Alabama in Huntsville. This session was centered around the changes faced by the Indian economy and the population following the 1991 economic reforms.

Through this session, Professor D’Costa presented an alternative approach to understanding the development dynamic of India. Through the use of capitalist dynamics in developing countries and compressed capitalism, Professor D’Costa showed that wealth inequality present in India is an inherent trait of late capitalist societies.

Overall, this session explained how some of the defining flaws of a capitalist society in a developing country are not an anomaly but rather a key tenet of a late capitalist society. The findings discussed in this session led to a broader understanding of some key tenets of capitalism. View here.

4. Designing a Pro-Market Social Protection System: A Literature Review

This session featured Professor Dr. Einar Øverbye, a Professor in International Social Welfare and Health Policy at Oslo Metropolitan University. This session was centered around the common argument that the welfare state is detrimental to the economy as it disincentivizes work.

Through this session, Professor Øverbye was able to explain and deconstruct the arguments surrounding the idea of welfare states disincentivizing work and reducing efficiency. By deconstructing the disincentive argument, Professor Øverbye was able to put forward his argument in support of designing a pro-market social protection system. Moreover, Professor Øverbye was able to demonstrate the importance of good design in a social system, thus unraveling the challenge surrounding the construction of a pro-market social protection system.

Overall, this session explained how good design in social structures can overcome some fundamental flaws associated with a system. This session also covered the role of a welfare state in a capitalist society and was able to discuss the contribution of key tenets of capitalism to a pro-market social protection system. View here.

5. The Law is an Anagram of Wealth

This session featured Professor Dr. Benjamin Davy, a visiting professor at the Faculty of Law, University of Johannesburg, and the School of Architecture and Spatial Planning, TU Wien University. Based on the book, “Land Policy”, this session addressed the relationship between land uses, land value, and land law.

Professor Davy was able to explain and demonstrate how the concept of material wealth depends heavily on the legal system present in a country. By using land laws and values, Professor Davy was able to explain how the economic structure of a society is affected by the law, thus leading back to the title of the session

Overall, this session showed attendees how material wealth, a key component of capitalism, depends on the legal system of a country. This inter-disciplinary session was also able to display the link between two seemingly unrelated fields of the social sciences, namely economics and law. View here.

6. John Stuart Mill’s Imperialism, Protestant Work Ethic, & Global South

This session featured Professor Dr. Elizabeth Anderson, the John Dewey Distinguished University Professor of Philosophy and Women’s & Gender Studies at the University of Michigan, Ann Arbor. This session was co-organized with Diana Soeiro, an organizer at the Philosophy of Economics Working Group. This session was based on the core ideas of Professor Anderson’s upcoming book, which is focused on the history of the Protestant work ethic through the history of economics.

Through this session, Professor Anderson was able to show how John Stuart Mill’s economic theories on workers and his liberal ideas were contradictory to his stance on Imperialism. Professor Anderson was able to trace Mill’s contradictions to tensions innate to the Protestant work ethic. By doing this, Professor Anderson was able to transition to a more global discussion of the Protestant work ethic, which would be able to address the challenges faced by workers in the Global South in today’s economy.

Overall, this session presented yet another interdisciplinary focus on capitalism through philosophy and work ethic. By linking Mill’s contrarian positions to tensions in the Protestant work ethic and by globalizing the topic to factor in worker challenges in the Global South, Professor Anderson was able to provide some key insights on the often-ignored role of work ethic and philosophy in capitalism and globalization.View here.

7. Why Poverty is More Than a Lack of Income: Thoughts from China

This session featured Professor Dr. Robert Walker MBE, Professor at the Institute of Social Management/School of Sociology, Beijing Normal University under China’s ‘High-Level Foreign Talents’ program. This session was centred around the contemporary understanding of poverty beyond income and the case of China, which attempted to eradicate poverty in the 2010s.

Through this session, Professor Walker was able to highlight the disparity between policy and political reality when it comes to the concept of poverty.

By including the case of China, which eliminated absolute poverty to discover the presence of relative poverty, Professor Walker was able to shift the argument of poverty beyond the idea of low income and was able to provide psychological insights on poverty.

Overall, this session presented the need to rethink the mainstream understanding of poverty. Discussions surrounding China’s attempts to eradicate poverty presented an undocumented side of China affected by the country’s shift towards a semi-capitalist society. This session also provided an interdisciplinary outlook on poverty in China, which allowed attendees from the South Asia Working Group to be cognizant of poverty conditions in other Asian regions. View here

8. Beyond False Dilemmas in Economic Policy

The final session of the first season featured Dr. Sanjay G. Reddy, Associate Professor of Economics at The New School for Social Research. This session was centred around the discussion of false dilemmas in economic policy.

Through this session, Dr. Reddy was able to present his economic argument for dissolving and dismissing false dilemmas rather than resolving them. By using the false dilemmas of “for or against growth” and “domestic markets or globalization”, Dr. Reddy proved the logical fallacy in such dilemmas and presented alternative questions that were worth pursuing.

Overall, this session provided closure for the first season of “Dissecting Capitalism” by discussing false dilemma, a prominent element found in the discourse and dialogue surrounding capitalism and the need to rethink it. By discussing the “for or against growth” dilemma, Dr. Reddy was able to discuss a core argument presented by people opposing the need to rethink capitalism. Ultimately, this session allowed the attendees to dissect capitalism through the notion of false dilemmas present in today’s economic world. View here

Over the course of 8 webinar series held across 2 months, the South Asia Working Group was able to embark on a journey of exploration, learning and profound thinking. Moreover, the attendees were able to actively discuss core ideas of capitalism and dissect capitalist structures and norms, which enhanced discussion within the working group.

While this season did cover mainstream ideas of capitalism and other economic factors that are affected by capitalism, it did not cover the link between capitalism and heterodox fields such as climate economics and agricultural economics. This is something that Season II aims to cover. With a wide range of topics from economic thought to climate change to legal theory, Season II aims to build upon the foundations of the first season and further continue to explore the tenets of capitalism.

Season II will feature Jayati Ghosh, Barbara Harris-White, Shailaja Fennell, Katharina Pistor, and K V Subramanian. Join us live!

The YSI South Asia Working Group provides a platform for young scholars from South Asia -or those interested in the region- to select an issue they wish to work on, collaborate and discuss for better conceptualization of the problem and, debate, critique and improve upon solutions. We also invite scholars to suggest the most pressing problems and challenges to better guide the path for this working group. Join us!

About the organizers:

Sattwick Dey Biswas is an affiliated Research Fellow at the Institute of Public Policy, Bangalore, India. In 2019, he has earned Doctor rerum politicarum at the School of Spatial Planning, TU Dortmund University, Germany. He has published his doctoral thesis as a book titled, “Land acquisition and compensation in India: Mysteries of valuation” (2020) with Palgrave Macmillan. He is interested in the areas of Land Policy, Social Policy, and Political Economy.

Shyam Soundararajan is a high school student from Dubai, UAE. His research interests include economic development, poverty and wealth inequality. He has published articles in the Harvard International Review and has contributed vastly to his school’s social science curriculum. Shyam aspires to major in Mathematical Economics with a minor in South Asian Studies.

Aneesha Chitgupi is a research fellow at the XKDR-Forum -Chennai Mathematical Institute. She received her PhD in 2020 from Institute for Social and Economic Change affiliated to University of Mysore. Her thesis analysed the economic determinants of India’s external stabilisation under the balance of payments framework. Her current research interests are public finance, government debt and liabilities management.

In her book fellow YSI member Birsen Filip makes an important and timely contribution by telling the story of neoliberalism and its dramatic rise over the past four decades. She traces its impact on our contemporary way of living, thinking, and being and in so doing demonstrates its elevation to a near law of nature that permeates nearly every aspect of our society. Many of us will be familiar with many aspects she touches upon, but it is galvanizing to see how deeply neo-liberal thinking has penetrated and reshaped our way of being.

Birsen starts by expounding the pillar upon which neo-liberal thinking rests: negative freedom (chapters 2 and 3). Friedrich Hayek and Friedman developed the idea of negative freedom by defining it as ‘freedom from coercion’ – the liberty to consume, produce and exchange voluntarily – which stands in contrast to positive freedom (i.e. improving individual self-determination by investing in individuals, communities, environments by the government). It purports that economic freedom in the marketplace (‘freedom to choose’) is a precondition for political and civic freedom (‘right to assembly, freedom of speech, freedom of religion’ etc). A threat or coercion on economic freedom would mean an infringement on political freedom as well. This expresses itself in the primacy of the marketplace, free individual choice, free fluctuation of prices and not allowing the government or any central entity to infringe on this economic freedom for an apparent collective good (freedom from coercion).

How this concept of freedom limits the scope of government is treated in chapter 4. Chapter 5 treats the rise of transnational corporations which have been able to take advantage of an ever-increasing scope of the market. In chapters 6 and 7 we vividly see the effect of mass consumption culture on the environment. How private interest stands over public interest in innovation policies is described in chapter 8. Chapter 9 and 10 illustrate the decline of unions and organized labor and the rise of inequality, and chapter 11 the decline of moral and ethical values. In chapter 12, Birsen returns to the realm of ideas to show how neo-liberal thinking has become entrenched with the academy.

At the core of the book’s message, Birsen demonstrates a disastrous paradox: the supposed freedom which neo-liberalism promotes is indeed a trap. What Birsen describes is a vortex in which more and more spheres of our lives become caught in. ‘Freedom from’ indeed is not indeed liberating. On the contrary, it is contributing to the decline of freedom; it imprisons and destroys our capacity for imagining alternative pathways and collective action and in doing so it destroys our ability as individuals and societies to confront our problems. We can all sense the writing on that wall, namely the steady decline and destruction of societies and our environment, and yes, of individual freedom.

What the book offers is how deeply neo-liberal ideas have taken hold of our thinking and penetrated how we perceive ourselves as individuals, how we relate with others. Moreso, it offers a glimpse of how we are eroding our social fabric and destroying our environment by extending the sphere of the market to nearly anything and exploiting the resources of our environment. More deeply it also sheds light on the current malaise and inability to address our global challenges since neo-liberal thinking discounts the ability of collective action (state and unions).

Birsen offers a hopeful plea that recognizing these entrappings which we all intuitively sense may help lead to a change in mindset and an affirmation vision of our global society and the environment in which we live: Positive freedom.

Birsen Filipholds a Ph.D. in philosophy and master’s degrees in economics and philosophy. She has published numerous articles and chapters on a range of topics, including political philosophy, geopolitics, and the history of economic thought, with a focus on the Austrian School of Economics and the German Historical School of Economics.

Jay Pocklington is the Manager of the Institute for New Economic Thinking’s Young Scholars Initiative (YSI). He received B.Sc. and M.Sc degrees in economics from Freie Universität Berlin.

By Elham Saeidinezhad | There is a consensus amongst the economist that the shadow banking system and the repurchase agreements (repos) have become the pinnacle of the dollar funding. In the repo market, access to liquidity depends on the firms’ idiosyncratic access to high-quality collateral, mainly U.S. Treasuries, as well as the systemic capacity to reuse collateral. Yet, the emergence of the repo market, which is considered an offshore credit system, and the expectations of higher inflation, have sparked debates about the demise of the dollar. The idea is that the repo market is becoming less attractive from an accounting and risk perspective for a small group of global banks, working as workhorses of the dollar funding network. The regulatory movement after the Great Financial Crisis (GFC), including leverage ratio requirements and liquidity buffers, depressed their ability to take counterparty risks, including that of the repo contracts. Instead, large banks are driven to reduce the costs of maintaining large balance sheets.

This note argues that the concerns about the future of the dollar might be excessive. The new monetary architecture does not structurally reduce the improtance of the U.S. government liabilities as the key to global funding. Instead, the traditional status of the dollar as the world’s reserve currency is replaced by the U.S. Treausies’ modern function as the world’s safest asset and the pinnacle of the repo market. Lastly, I put the interactions between the Fed’s roles as the manager of the government’s debt on the one hand and monetary policy architect on the other at the center of the analysis. Recognizing the interconnectedness could deepen our understanding of the Fed’s control over U.S. Treasuries.

As a result of the Bretton Woods Agreement, the dollar was officially crowned the world’s reserve currency. Instead of gold reserves, other countries accumulated reserves of dollars, the liability of the U.S. government. Till the mid-1980s, the dollar was at the top of the monetary hierarchy in both onshore and offshore financial systems. In the meantime, the dollar’s reserve status remained in an natural way. Outside the U.S., a few large global banks were supplying dollar funding to the rest of the world. This offshore bank-oriented system was called the Eurodollar market. In the U.S., the Federal Funds market, an interbank lending market, became the pinnacle of the onshore dollar funding system. The Fed conducted a simple monetary policy, detached from the capital market, and managed exclusively within the traditional banking system.

Ultimately, events never quite followed this smooth pattern, which in retrospect may not be regretted. The growth of shadow banking system meant that international investors reduced their reliance on bank loans in the Eurodollar markte. Instead, they turned to the repo market and the FX swaps market. In the U.S., the rise of the repo market implied that the U.S. monetary policy should slowly leak into capital market and directly targe the security dealers. At the heart of this structural break was the growing acceptance of the securities as collaterals.

Classical monetary economics proved to be handicapped in detecting this architectural development. According to theories, the supply of the dollar is determined in the market for the loanable funds where large banks act as financial intermediaries and stand between savers and borrowers. In the process, they set the price of the dollar funding. Regarding the global value of the dollar, as long as the Fed’s credibility in stabilizing prices exceeds its peers, and Treasury keeps its promises to pay, the global demand for the dollar will be significant. And the dollar will maintain its world reserve currency status. These models totally overlooked the role of market-makers, also called dealers, in providing short-term liquidity. However, the rise of the shadow banking system made such an abstraction a deadly flaw. In the new structure, the dealers became the de facto providers of the dollar funding.

Shadow banking created a system where the dealers in the money market funded the securities lending activities of the security dealers in the capital market. This switch from traditional banking to shadow banking unveiled an inherent duality in the nature of the Fed. The Fed is tasked to strike a balance between two rival roles: On the one hand, the Fed is the Treasury’s banker and partially manages U.S. debt. On the other hand, it is the bankers’ bank and designs monetary policy. After the financial crises of the 1980s and 1990s, the Fed tried to keep these roles divided as separate arms of macroeconomic policy. The idea was that the links between U.S. debt management and liquidity are weak, as the money market and capital market are not interconnected parts of the financial ecosystem. This weak link allowed for greater separation between monetary policy and national debt management.

The GFC shattered this judgment and exposed at least two features of shadow banking. First, in the new structure, the monetary condition is determined in the repo market rather than the banking system. The repo market is very large and the vast majority of which is backed by U.S. Treasuries. This market finances the financial market’s primary dealers’ large holdings of fixed-income securities. Second, in the new system, U.S. Treasuries replaced the dollar. The repo instruments are essentially short-term loans secured by liquid “collateral”. Although hedge funds and other types of institutional investors are important suppliers of collateral, the single most important issuer of high quality, liquid collateral, is the U.S. Treasury.

U.S. Treasury securities have become the new dollar. Hence, its velocity began to matter. The velocity of collateral, including U.S. Treasuries, is the ratio of the total pledged collateral received by the large banks (that is eligible to be reused), divided by the primary collateral (ie, sourced via reverse repos, securities borrowing, prime brokerage, and derivative margins). Before the GFC, the use (and reuse) of pledged collateral was comparable with the velocity of monetary aggregates like M2. The “reusability” of the collateral became instrumental to overcome the good collateral deficit.

After the GFC, the velocity of collateral shrank due to the Fed’s QE policies (involving purchases of bonds) and financial regulations that restricted good collateral availability. Nontheless, the availability of collateral surpassed the importance of private credit-creation in the traditional banking system. It also started to leak into the monetary policy decision-making process as the Fed started to consider the Treasury market condition when crafting its policies. At first glance, the Treasury market’s infiltration into monetary policy indicates a structural shift in central banking. First, the Treasury market is a component of the capital market, not the money market. Second, the conventional view of the Fed’s relationship with the Treasury governs that its responsibilities are mainly limited to managing the Treasury account at the Fed, running auctions, and acting as U.S. Treasuries registrar.

However, a thorough study of the traditional monetary policy would paint a different picture of the Fed and the U.S. Treasuries. Modern finance is only making the Fed’s role as a de-facto U.S. national debt manager explicit. The Fed’s primary monetary policy tool, the open market operation, is essentially monetizing national debt. Essentially, the tool enabled the Fed to monetize some portion of the national debt to control the quantity of bank reserves. The ability to control the level of bank reserves permitted the Fed to limit the level of bank intermediation and private credit creation. This allowed the Fed to focus on compromising between two objectives of price stability and full employment.

What is less understood is that the open market operation also helped the Fed’s two roles, Treasury’s bank and the bankers’ bank, to coexist privately. As private bankers’ bank, the Fed designs monetary policy to control the funding costs. As the Treasury’s bank, the Fed is implicitly responsible for U.S. debt management. The open market operation enabled the Fed to control money market rates while monetizing some portion of the national debt. The traditional monetary system simply helped the Fed to conceal its intentions as Treasury’s bank when designing monetary policy.

The point to emphasize is that the traditional central banking was only hiding the Fed’s dual intentions. The Fed could in theory monetize anything— from gold to scrap metals—but it has stuck largely to Treasury IOUs. One reason is that, unlike gold, there has never been any shortage of them. Also, they are highly liquid so the Fed can sell them with as much ease as it buys them. But, a third, and equally important reason is that in doing so, the Fed explicitly fulfilled its “role” as the manager of the U.S. national debt. All this correctly suggests that the Fed, despite its lofty position at the pinnacle of the financial system, has always been, and is, none other than one more type of financial intermediary between the government and the banking system.

The high-level relationship between the Treasury and the Fed is “inherent” and at the heart of monetary policy. Yet, nowhere along the central banking learning curve has been a meaningful examination of the right balances between the Fed’s two roles. The big assumption has been that these functions are distinctly separated from each other. This hypothesis held in the past when the banks stood between savers and borrowers as financial intermediaries. In this pre-shadow banking world, the money market and capital market were not interconnected.

Yet, the GFC revealed that more than 85 percent of the lending was based on securities lending and other credit products, including the repo. In repo, broker-dealers, hedge funds, and banks construct short-term transactions. They put up collateral—mostly U.S. Treasury securities —with an agreement to buy them back the next day or week for slightly more, and invest the proceeds in the interim. The design and conduct of the monetary policy intimately deepened on the availability and price of the U.S. Treasuries, issues at the heart of the U.S. national debt management.

The U.S. debt management and monetary policy reunion happened in the repo market. In a sense, repo is a “reserve-less currency system,” in the global funding supply chain. It is the antithesis of the reserve currency. In traditional reserve currency, central banks and major financial institutions hold a large amount of currency to use for international transactions. It is also ledger money which indicates that the repo transactions, including the securities lending of its, are computed digitally by the broker-dealers. The repo market is a credit-based system that is a reserve-less, currency-less form of ledger money.

In this world of securities lending, which has replaced traditional bank lending, the key instrument is not the dollar but the U.S. Treasury securities that are used as collateral. The U.S. national debt is being used to secure funding for private institutional investors. Sometimes lenders repledge them to other lenders and take out repo loans of their own. And the cycle goes on. Known as rehypothecation, these transfers used to be done once or twice for each posted asset but are now sometimes done six to eight times, each time creating a new money supply. This process is the de-facto modern money creation—and equally depends on the Fed’s role as Treasury’s bank and bankers’ bank.

Understanding how modern money creation works has implications for the dollar’s status in the international monetary system. Some might argue that the dollar is losing its status as the global reserve currency. They refer to the collateralized repo market and argue that this market allows international banks operating outside the supervision of the Fed to create US dollar currency. Hence, the repo, not the dollar, is the real reserve currency. Such statements overlook the repo market’s structural reliance on the U.S. Treasury securities and neglect the Fed’s role as the de-facto manager of these securities. Shadow banking merely replaced the dollar with the U.S. Treasuries as the world’s key to funding gate. In the meantime, it combined the Fed’s two roles that used to be separate. Indeed, the shadow banking system has increased the importance of U.S. institutions.

The rising dominance of the repo market in the global funding supply chain, and the decline in collateral velocity, implies that the viability of the modern Eurodollar system depends on the U.S. government’s IOUs more than any time in history. US Treasuries, the IOU of the US government, is the most high-quality collateral. When times are good, repos work fine: The agreements expire without problems and the collateral gets passed back down the chain smoothly. But eventually, low-quality collateral lurks into the system. That’s fine, until markets hit an inevitable rough patch, like, March 2020 “Dash for Cash” episode. We saw this collateral problem in action. In March credit spreads between good and junkier debt widened and Treasury prices spiked as yields plummeted because of the buying frenzy. The interest rate on one-month Treasurys dropped from 1.61% on Feb. 18 to 0.00% on March 28. That was the scramble for good collateral. The reliance on the repo market to get funding indicates that no one will take the low-quality securities, and everyone struggles for good collateral. So whenever uncertainty is high, there will be a frenetic dash to buy Treasurys—like musical chairs with six to eight buyers eagerly eyeing one chair.

Elham Saeidinezhad is a Term-Assistant Professor of Economics at Barnard College, Columbia University. Before joining Barnard College, she was a lecturer of Economics at UCLA, a research economist in the International Finance and Macroeconomics research group at Milken Institute, Santa Monica, and a postdoctoral fellow at the Institute for New Economic Thinking (INET), New York. As a postdoctoral fellow, Elham worked closely with Prof. Perry Mehrling and studied his “Money View” framework. She obtained my Ph.D. from the University of Sheffield, UK, in empirical Macroeconomics in 2013. You may contact Elham via the Young Scholars Directory

Liquidity transformation is a crucial function for many banks and non-bank financial intermediaries. It is a balance sheet operation where the firm creates liquid liabilities financed by illiquid assets. However, liquidity transformation is a risky operation. For policymakers and macroeconomists, the main risk is to financial stability caused by systemic liquidation of assets, also called “firesale.” In this paper, I emphasize an essential characteristic of firesale that is less explored—the order of liquidation. The order of liquidation refers to the sequence at which financial assets are converted into cash or cash equivalents- when the funds face significant cash outflow. Normally, economists explain assets’ order of liquidation by using theories of capital structure. However, the financial market episodes, such as March 2020 “Cash for Dash,” have revealed that firms’ behaviors are not in line with the predictions of such classical theories. Capital structure theories, such as “Pecking Order” and “Trade-off,” argue that fund managers should use their cash holding as the first line of defense during a liquidity crunch before selling their least liquid asset. In contrast to such prophecies, during the recent financial turmoil, funds liquidated their least liquid assets, even US Treasuries, first, before unhoarding their cash and cash equivalents. In this paper, I explore a few reasons that generated the failure of these theories when explaining funds’ behavior during a liquidity crisis. I also explain why Money View can be used to build an alternative framework.

Traditional capital structure theories such as pecking order differentiate financial assets based on their “adverse selection” and “information costs” rather than their “liquidity.” The pecking order theory is from Myers (1984) and Myers and Majluf (1984). Since it is famous, I will be brief. Assume that there are two funding sources available to firms whenever they hit their survival constraint: cash (or retained earnings) and securities (including debt and equity). Cash has no “adverse selection” problem, while securities, primarily equity, are subject to serious adverse selection problems. Compared to equity, debt securities have only a minor adverse selection problem. From the point of view of an external investor, equity is strictly riskier than debt. Both have an adverse selection risk premium, but that premium is significant on equity. Therefore, an outside investor will demand a higher rate of return on equity than on debt. From the perspective of the firm’s managers, the focus of our paper, cash is a better source of funds than is securities. Accordingly, the firm would prefer to fund all its payments using “cash” if possible. The firm will sell securities only if there is an inadequate amount of cash.

In the trade-off theory, another popular conventional capital structure theory, a firm’s decision is a trade-off between tax-advantage and capital-related costs. In a world that firms follow trade-off theory, their primary consideration is a balance between bankruptcy cost and tax benefits of debt. According to this approach, the firm might optimize its financing strategies, including whether to make the payments using cash or securities, by considering tax and bankruptcy costs. In most cases, these theories suggest that the firms prefer to use their cash holdings to meet their financial obligations. They use securities as the first resort only if the tax benefit of high leverage exceeds the additional financial risk and higher risk premiums. The main difference between pecking order theory and trade-off theory is that while the former emphasizes the adverse selection costs, the latter highlights the high costs of holding extra capital. Nonetheless, similar to the pecking order theory, the trade-off theory predicts that firms prefer to use their cash buffers rather than hoarding them during a financial crisis.

After the COVID-19 crisis, such predictions became false, and both theories underwent a crisis of their own. A careful examination of how funds, especially intermediaries such as Money Market Funds, or MMFs, adjusted their portfolios due to liquidity management revealed that they use securities rather than cash as the first line of defense against redemptions. Indeed, such collective behavior created the system-wide “dash for cash” episode in March 2020. On that day, few funds drew down their cash buffers to meet investor redemptions. However, contrary to pecking order and trade-off theories, most funds that faced redemptions responded by selling securities rather than cash. Indeed, they sold more of the underlying securities than was strictly necessary to meet those redemptions. As a result, these funds ended March 2020 with higher cash levels instead of drawing down their cash buffers.

Such episodes cast doubt on the conventional theories of capital structure for liquidity management, which argues that funds draw on cash balances first and sell securities only as a last resort. Yet, they align with Money View’s vision of the financial hierarchy. Money View asserts that during the financial crisis, preservation of cash, the most liquid asset located at the top of the hierarchy, will be given higher priority. During regular times, the private dealing system conceals such priorities. In these periods, the private dealing system uses its balance sheets to absorb trade imbalances due to the change in preferences to hold cash versus securities. Whenever the demand for cash exceeds that of securities, the dealers maintain price continuity by absorbing the excess securities into their balance sheets. Price continuity is a characteristic of a liquid market in which the bid-ask spread, or difference between offer prices from buyers and requested prices from sellers, is relatively small. Price continuity reflects a liquid market. In the process, they can conceal the financial hierarchy from being in full display.

During the financial crisis, this hierarchy will be revealed for everyone to see. In such periods, the dealers cannot or are unwilling to use their job correctly. Due to the market-wide pressing need to meet payment obligations, the trade imbalances show up as an increased “qualitative” difference between cash and securities. In the course of this differentiation, there is bound to be an increase in the demand for cash rather than securities, a situation similar to the “liquidity trap.” A liquidity trap is a situation, described in Keynesian economics, in which, after the rate of interest has fallen to a certain level, liquidity preference may become virtually absolute in the sense that almost everyone prefers holding cash rather than holding a debt which yields so low a rate of interest. In this environment, investors would prefer to reduce the holding of their less liquid assets, including US Treasuries, before using their cash reserves to make their upcoming payments. Thus, securities will be liquidated first, and cash will be used only as a last resort.

The key to understanding such behaviors by funds is recognizing that the difference in the quality of the financial instruments’ issuers creates a natural hierarchy of financial assets. This qualitative difference will be heightened during a crisis and determines the capital structure of the funds, and the “order of liquidation” of the assets, for liquidity management purposes. When the payments are due and liquidity is scarce, firms sell illiquid assets ahead of drawing down the cash balances. In the process, they disrupt money markets, including repo markets, as they put upward pressure on the price of cash in terms of securities. Thus, during a crisis, the liability of the central banks becomes the most attractive asset to own. On the other hand, securities, the IOUs of the private sector, become the less desirable asset to hold for asset managers.

So why do standard theories of capital structure fail to explain firms’ behavior during a liquidity crisis? First, they focus on the “fallacious” type of functions and costs during a liquidity crunch. While the dealers’ “market-making” function and liquidity are at the heart of Money View, the standard capital structure theories stress the “financial intermediation” and “adverse selection costs.” In this world, the “ordering” of financial assets to be liquidated may stem from sources such as agency conflicts and taxes. For Money View, however, what determines the order of firesaled assets, and the asset managers’ portfolio is less the agency costs and more the qualitative advantage of one asset than another. The assets’ status determines such qualitative differences in the financial hierarchy. By disregarding the role of dealers, standard capital structure models omit the important information that the qualitative difference between cash and credit will be heightened, and the preference will be changed during a crisis.

Such oversight, mixed with the existing confusion about the non-bank intermediaries’ business model, will be fatal for understanding their behavior during a crisis. The difficulty is that standard finance theories assume that non-bank intermediaries, such as MMFs, are in the business of “financial intermediation,” where the risk is transferred from security-rich agents to cash-rich ones. Such an analysis is correct at first glance. However, nowadays, the mismatch between the preferences of borrowers and the preferences of lenders is increasingly resolved by price changes rather than by traditional intermediation. A careful review of the MMFs balance sheets can confirm this viewpoint. Such examination reveals that these funds, rather than transforming the risks, “pool” them. Risk transformation is a defining characteristic of financial intermediation. Yet, even though it appears that an MMF is an intermediary, it is mainly just pooling risk through diversification and not much transforming risk.

Comprehending the MMF’s business as pooling the risks rather than transforming them is essential for understanding the amount of cash they prefer to hold. The MMF shares have the same risk properties as the underlying pool of bonds or stocks by construction. There is some benefit for the MMF shareholders from diversification. There is also some liquidity benefit, perhaps because open-end funds typically promise to buy back shares at NAV. But that means that MMFs have to keep cash or lines of credit for the purpose, even though it will lower their return and increase the costs for the shareholders.

Finally, another important factor that drives conventional theories’ failure is their concern about the cash flow patterns in the future and the dismissal of the cash obligations today. This is the idea behind the discounting of future cash flows. The weighted average cost of capital (WACC), generally used in these theories, is at the heart of discounting future cash flows. In finance, discounted cash flow analysis is a method of valuing security, project, company, or asset using the time value of money. Discounted cash flow analysis is widely used in investment finance, real estate development, corporate financial management, and patent valuation. In this world, the only “type” of cash flow that matters is the one that belongs to a distant future rather than the present, when firms should make today’s payments. On the contrary, the present, not the future, and its corresponding cash flow patterns, is what Money View is concerned about. In Money View’s world, the firm should be able to pay its daily obligations. If it does not have continuous access to liquidity and cannot meet its cash commitments, there will be no future.

The pecking order theory derives much of its influence from a view that it fits naturally with several facts about how companies use external finance. Notably, this capital structure theory derives support from “indirect” sources of evidence such as Eckbo (1986). Whenever the theories are rejected, the conventional literature usually attributes the problem to cosmetic factors, such as the changing population of public firms, rather than fundamental ones. Even if the pecking order theory is not strictly correct, they argue that it still does a better job of organizing the available evidence than other theories. The idea is that the pecking order theory, at its worst, is the generalized version of the trade-off theory. Unfortunately, none of these theories can explain the behavior of firms during a crisis, when firms should rebalance their capital structure to manage their liquidity needs.

The status of classical theories, despite their failures to explain different crises, is symptomatic of a hierarchy in the schools of economic thought. Nonetheless, they are unable to provide strong capital structure theories as they focus on fallacious premises such as the adverse selection or capital costs of an asset. To build theories that best explain the financing choices of corporates, economists should emphasize the hierarchical nature of financial instruments that reliably determines the order of liquidation of financial assets. In this regard, Money View seems to be positioned as an excellent alternative to standard theories. After all, the main pillars of this framework are financial hierarchy, dealers, and liquidity management.

Elham Saeidinezhad is a Term-Assistant Professor of Economics at Barnard College, Columbia University. Before joining Barnard College, she was a lecturer of Economics at UCLA, a research economist in the International Finance and Macroeconomics research group at Milken Institute, Santa Monica, and a postdoctoral fellow at the Institute for New Economic Thinking (INET), New York. As a postdoctoral fellow, Elham worked closely with Prof. Perry Mehrling and studied his “Money View” framework. She obtained my Ph.D. from the University of Sheffield, UK, in empirical Macroeconomics in 2013. You may contact Elham via the Young Scholars Directory

Every so often, we highlight one of the members of the YSI community to share their story and aspirations. Today we cover Petronella Munhenzva, coordinator of the Africa Working Group. This year, Petronella is launching not just a book but also a foundation to support students in Gokwe (Zimbabwe) where she grew up. We talked to her about her hopes, dreams, and where she got the courage to dream.

What led you to decide to write From Gokwe to Oxford?

During my first couple of weeks at Oxford, an American girl came up to me and asked me where I was from. So I told her I’m from Zimbabwe and immediately she went “oh, from Harare I guess?” When I told her no, she thought that was very impressive. The whole interaction was a bit odd to me, but I didn’t think too much of it.

But then those conversations kept on repeating. It turned out I was the only black graduate student at my college, and every time I got questions about my background, everyone was taken aback. They thought I must be a princess. Or a diplomat’s daughter who went to private school in the US.

So I realized I had a choice to make. One option was to go along with the expectations that people had and walk around like an African princess. And I wouldn’t be the first! I know people who tweak their accent and might even lie about what their parents do. But it wouldn’t be the truth, and it would deny the fact that there is real talent and potential in places like Gokwe. It would perpetuate the divide between those who have resources and those who don’t.

So I decided to embrace my story and explain that YES, someone who went to school in a forgotten part of Zimbabwe can go straight to Oxford.Because guess what? People there are smart and talented, too! Both the people at Oxford and the people in Gokwe should realize that.

Tell us about the foundation.

I realized the book would be a starting point; a way to rekindle hopes and dreams. But real resources are needed, too. Gokwe is one of the least developed areas in Zimbabwe. Leaking roofs. Potholes in the road. No money for school. I was there again in December and talked with some of my friends that I met growing up and went to school with. And we just reflected on this sense that most people can never get out of there. So the first thing to do is to believe that things can get better; that’s what the book is for. The second thing is to make them better; that’s where the foundation comes in.

My long term vision is to pay for as many kids’ school fees as possible. And it doesn’t take much! I went to six different schools in Gokwe and guess how much the most expensive one was? 15 US dollars per term. Same with uniforms. They’re made of fabric that’s about 80 cents a meter, so with three dollars you have a uniform. So I want to make sure children stay in school, they have the basic materials they need, and give them access to projects that can develop their talents.

These are simple things. But they make the biggest difference in the world. Once, when I was working as a substitute teacher at my old school, we took a few students for a football tournament. And in our area, all the roads would be gravel with potholes everywhere – just terrible infrastructure. But when we got to a tarred road, one of my students suddenly started screaming. He was just SO excited to play football at a better facility for once. It looked like it was the best day of his life. But that was it. After one fun day everyone goes back home and the cycle continues.

And this keeps their dreams very limited. If you ask a Gokwe student what they want to be when they grow up, many of them just laugh. They don’t even know what you’re talking about! All they know is that when they grow up, they’re going to farm. Like their parents, with their cattle, have their crops. And there’s nothing wrong with being a farmer! But it should be a choice – not the only option.

But when you were little, there was no Petronella to help you! Who was your source of encouragement and support?

My parents – they are the best people in the world. We never really had much growing up but my dad Ronald was a high school teacher at a Gokwe school, and he was always talking about how important education is. He would make sure that you studied. He understood the value of education and working hard. He made sure you got your homework done. And he was extremely supportive of my dreams.

I remember one time when I was in primary school, my teacher told him I’d been doing well at English. So he picked up on that and started telling me I could become an English major! But he didn’t just say that. He started calling me “his English major.” And then when I got older, I wanted to become a lawyer. And he responded by calling me advocate. I was his “Advocate P!”. Then at another instance I decided I would apply for an exchange program with Sweden and after telling him about it, guess what he called me? Sister Sweden! And when I said I’d apply to Oxford? His Oxford Grad. Every time, he crystalized my dreams for me, and made them real before I’d even started. It’s a superpower.

October 2021 will bring not only the publication of From Gokwe to Oxford but also the launch of the Petronella Munhenzva Foundation. Learn more and become a supporter hereor contribute via the GoFundMe campaign.

Who has access to cheap credit? And who does not? Compared to small businesses and households, global banks disproportionately benefited from the Fed’s liquidity provision measures. Yet, this distributional issue at the heart of the liquidity provision programs is excluded from analyzing the recession-fighting measures’ distributional footprints. After the great financial crisis (GFC) and the Covid-19 pandemic, the Fed’s focus has been on the asset purchasing programs and their impacts on the “real variables” such as wealth. The concern has been whether the asset-purchasing measures have benefited the wealthy disproportionately by boosting asset prices. Yet, the Fed seems unconcerned about the unequal distribution of cheap credits and the impacts of its “liquidity facilities.” Such oversight is paradoxical. On the one hand, the Fed is increasing its effort to tackle the rising inequality resulting from its unconventional schemes. On the other hand, its liquidity facilities are being directed towards shadow banking rather than short-term consumers loans. A concerned Fed about inequality should monitor the distributional footprints of their policies on access to cheap debt rather than wealth accumulation.

Dismissing the effects of unequal access to cheap credit on inequality is not an intellectual mishap. Instead, it has its root in an old idea in monetary economics- the quantity theory of money– that asserts money is neutral. According to monetary neutrality, money, and credit, that cover the daily cash-flow commitments are veils. In search of the “veil of money,” the quantity theory takes two necessary steps: first, it disregards the payment systems as mere plumbing behind the transactions in the real economy. Second, the quantity theory proposes the policymakers disregard the availability of money and credit as a consideration in the design of the monetary policy. After all, it is financial intermediaries’ job to provide credit to the rest of the economy. Instead, monetary policy should be concerned with real targets, such as inflation and unemployment.

Nonetheless, the reality of the financial markets makes the Fed anxious about the liquidity spiral. In these times, the Fed follows the spirit of Walter Bagehot’s “lender of last resort” doctrine and facilitates cheap credits to intermediaries. When designing such measures, the Fed’s concern is to encourage financial intermediaries to continue the “flow of funds” from the surplus agents, including the Fed, to the deficit units. The idea is that the intermediaries’ balance sheets will absorb any mismatch between the demand-supply of credit. Whenever there is a mismatch, a financial intermediary, traditionally a bank, should be persuaded to give up “current” cash for a mere promise of “future” cash. The Fed’s power of persuasion lies in the generosity of its liquidity programs.

The Fed’s hyperfocus on restoring intermediaries’ lending initiatives during crises deviates its attention from asking the fundamental question of “whom these intermediaries really lend to?” The problem is that for both banks and non-bank financial intermediaries, lending to the real economy has become a side business rather than a primary concern. In terms of non-bank intermediaries, such as MMFs, most short-term funding is directed towards shadow banking businesses of the global banks. Banks, the traditional financial intermediaries, in return, use the unsecured, short-term liquidity to finance their near-risk-free arbitrage positions. In other words, when it comes to the “type” of borrowers that the financial intermediaries fund, households, and small-and-medium businesses are considered trivial and unprofitable. As a result, most of the funding goes to the large banks’ lucrative shadow banking activities. The Fed unrealistically relies on financial intermediaries to provide cheap and equitable credit to the economy. In this hypothetical world, consumers’ liquidity requirements should be resolved within the banking system.

This trust in financial intermediation partially explains the tendency to overlook the equitability of access to cheap credit. But it is only part of the story. Another factor behind such an intellectual bias is the economists’ anxiety about the “value of money” in the long run. When it comes to the design of monetary policy, the quantity theory is obsessed by the notion that the only aim of monetary theory is to explain those phenomena which cause the value of money to alter. This tension has crept inside of modern financial theories. On the one hand, unlike quantity theory, modern finance recognizes credit as an indispensable aspect of finance. But, on the other hand, in line with the quantity theory’s spirit, the models’ main concern is “value.”

The modern problem has shifted from explaining any “general value” of money to how and when access to money changes the “market value” of financial assets and their issuers’ balance sheets. However, these models only favor a specific type of agent. In this Wicksellian world, adopted by the Fed, agents’ access to cheap credit is essential only if their default could undermine asset prices. Otherwise, their credit conditions will be systemically inconsequential, hence neutral. By definition, such an agent can only be an “institutional” investor who’s big enough so that its financial status has systemic importance. Households and small- and medium businesses are not qualified to enter this financial world. The retail depositors’ omission from the financial models is not a glitch but a byproduct of mainstream monetary economics.

The point to emphasize is that the Fed’s models are inherently neutral about the distributional impacts of credit. They are built on the idea that despite retail credit’s significance for retail payment systems, their impacts on the economic transactions are insignificant. This is because the extent of retail credit availability does not affect real variables, including output and employment, as the demand for this “type” of credit will have proportional effects on all prices stated in money terms. On the contrary, wholesale credit underpin inequality as it changes the income and wealth accumulated over time and determines real economic activities.

The macroeconomic models encourage central bankers to neglect any conditions under which money is neutral. The growing focus on inequality in the economic debate has gone hand in hand to change perspective in macroeconomic modeling. Notably, recent research has moved away from macroeconomic models based on a single representative agent. Instead, it has focused on frameworks incorporating heterogeneity in skills or wealth among households. The idea is that this shift should allow researchers to explore how macroeconomic shocks and stabilization policies affect inequality.

The issue is that most changes to macroeconomic modeling are cosmetical rather than fundamental. Despite the developments, the models still examine inequality through income and wealth disparity rather than equitable access to cheap funding. For small businesses and non-rich consumers, the models identify wealth as negligible. Nonetheless, they assume the consumption is sensitive to income changes, and consumers react little to changes in the credit conditions and interest rates. Thus, in these models, traditional policy prescriptions change to target inequality only when household wealth changes.

At the heart of the hesitation to seriously examine distributional impacts of equitable access to credit is the economists’ understanding that access to credit is only necessary for the day-to-day operation of the payments system. Credit does not change the level of income and wealth. In these theories, the central concern has always been, and is, solvency rather than liquidity. In doing so, these models dismiss the reality that an agent’s liquidity problems, if not financed on time and at a reasonable price, could lead to liquidations of assets and hence insolvency. In other words, retail units’ access to credit daily affects not only the retail payments system but also the units’ financial wealth. Even from the mainstream perspective, a change in wealth level would influence the level of inequality. Furthermore, as the economy is a system of interlocking balance sheets in which individuals depend on one another’s promises to pay (financial assets), their access to funding also determines the financial wealth of those who depend on the validations of such cash commitments.

Such a misunderstanding about the link between credit accessibility and inequality is a natural byproduct of macroeconomic models that omit the payment systems and the daily cash flow requirement. Disregarding payment systems has produced spurious results about inequality. In these models, access to liquidity, and the smooth payment systems, is only a technicality, plumbing behind the monetary system, and has no “real” effects on the macroeconomy.

The point to emphasize is that everything about the payment system, and access to credit, is “real”: first, inthe economy as a whole, there is a pattern of cash flows emerging from the “real” side, production and consumption, and trade. A well-functioning financial market enables these cash flows to meet the cash commitments. Second, at any moment, problems of mismatch between cash flows and cash commitments show up as upward pressure on the short-term money market rate of interest, another “real” variable.

The nature of funding is evolving, and central banking is catching up. The central question is whether actual cash flows are enough to cover the promised cash commitments at any moment in time. For such conditions to be fulfilled, consumers’ access to credit is required. Otherwise, the option is to liquidate accumulations of assets and a reduction in their wealth. The point to emphasize is that those whose access to credit is denied are the ones who have to borrow no matter what it costs. Such inconsistencies show up in the money market where people unable to make payments from their current cash flow face the problem of raising cash, either by borrowing from the credit market or liquidating their assets.

The result of all this pushing and pulling is the change in the value of financial wealth, and therefore inequality. Regarding the distributional effects of monetary policy, central bankers should be concerned about the effects of monetary policy on unequal access to credit in addition to the income and wealth distribution. The survival constraint, i.e., agents’ liquidity requirements to meet their cash commitments, must be met today and at every moment in the future.

To sum up, in this piece, I revisited the basics of monetary economics and draw lessons that concern the connection between inequality, credit, and central banking. Previously, I wroteabout the far-reaching developments in financial intermediation, where non-banks, rather than banks, have become the primary distributors of credit to the real economy. However, what is still missing is the distributional effects of the credit provision rather than asset purchasing programs. The Fed tends to overlook a “distributional” issue at the heart of the credit provision process. Such an omission is the byproduct of the traditional theories that suggest money and credit are neutral. The traditional theories also assert that the payment system is a veil and should not be considered in the design of the monetary policy. To correct the course of monetary policy, the Fed has to target the recipients of credit rather than its providers explicitly. In this sense, my analysis is squarely in the tradition of what Schumpeter (1954) called “monetary analysis” and Mehrling (2013) called “Money View” – the presumption that money is not a veil and that understanding how it functions is necessary to understand how the economy works.

Elham Saeidinezhad is lecturer in Economics at UCLA. Before joining the Economics Department at UCLA, she was a research economist in International Finance and Macroeconomics research group at Milken Institute, Santa Monica, where she investigated the post-crisis structural changes in the capital market as a result of macroprudential regulations. Before that, she was a postdoctoral fellow at INET, working closely with Prof. Perry Mehrling and studying his “Money View”. Elham obtained her Ph.D. from the University of Sheffield, UK, in empirical Macroeconomics in 2013. You may contact Elham via the Young Scholars Directory

The Fed is banking on non-bank intermediaries, such as money market funds (MMFs), rather than banks for monetary normalization. The short-term funding market reset after the famous FOMC meeting on June 16, 2021. The Fed explicitly brought forward forecasts for tighter monetary policy and boosted inflation projections. However, it is essential to understand what lies beneath the Fed’s message. Examining the “timing” of the Fed’s normalization and the primary “beneficiaries” unveils a modified FRB/US model to include the structural change in the intermediation business. Non-bank intermediaries, including MMFs, have become primary lenders in the housing market and accept deposits. In doing so, they have replaced banks as credit providers to the economy and have boosted their role in transmitting monetary policy. Following the pandemic, the timing of the Fed’s policies can be explained by the MMFs’ balance sheet problems. This shift in the Fed’s focus towards non-bank intermediaries has implications for the banks. Even though normalization tactics are universally strengthening MMFs, there are creating liability problems for the banking system.

A long-standing trend in macro-finance, the increased presence of the MMFs in the market for loanable funds, alters the Fed’s FRB/US model and informs this decision. The FRB/US model, in use by the Fed since 1996, is a large-scale model of the US economy featuring optimizing behavior by households and firms and detailed descriptions of the real economy and the financial sector. One distinctive feature of the Fed’s model compared to dynamic stochastic general equilibrium (DSGE) models is the ability to switch between alternative assumptions about economic agents’ expectations formation and roles. When it comes to the critical question of “who funds the real economy?” it is sensible to assume that non-bank financial entities, including MMFs, have replaced banks to manage deposits and lend. On their liabilities side, MMFs have become the savers’ de-facto money managers. This industry looks after $4tn of savings for individuals and businesses. On their asset sides, they have become primary lenders in significant markets such as housing, where the Fed keeps a close watch on.

Traditionally, two essential components of the FRB/US model, the financial market and the real economy, depended on the banks lending behavior. The financial sector is captured through monetary policy developments. Monetary policy was modeled as a simple rule for the federal funds rate, an interbank lending rate, subject to the zero lower bound on nominal interest rates. A variety of interest rates, including conventional 30-year residential mortgage rates, assumed to be set by the banks’ lending activities, informs the “federal funds target.” To capture aggregate economic activity, the FRB/US model assumed the level of spending in the model depends on intermediate-term consumer loan rates, again set by the banking system. The recent FOMC announcement sent a strong signal that the FRB/US model has been modified to capture the fading role of the banks in funding the economy and setting the rates.

One of the factors behind the declining role of the banking system in financing the economy is the depositors’ inclination to leave banks. Notably, most of this institutional run on the banking system is self-inflicted. After the pandemic, the Fed and government stimulus packages pointed to an influx of deposits. The problem is that banks’ balance sheet constraints have made managing deposits a costly business for the banks. First, the scarcity of balance sheet space implies banks have to forgo the more lucrative and unorthodox business opportunities if they accept deposits. Second, as the size of banks’ balance sheets increases, banks are required to hold more capital. Capital is expensive as it reduces banks’ returns on equity. These prudential requirements are more binding for the large, cash-rich banks. Post COVID-19 pandemic, cash-rich banks advised corporate clients to move money out of their firms and deposit them in MMFs. Pushing deposits into MMFs was preferable as it would reduce the size of banks’ balance sheets. The idea was that asset managers, who are not under the Fed’s regulatory radar, would be able and willing to manage the liquidity.

Effectively, bankers orchestrated run on their own banks by turning away deposits. Had the Fed overlooked such “unnatural” actions by banks, they could undermine financial stability in the long run. Therefore, after the COVID-19 pandemic, the Fed expanded access to the reverse repo programs to include non-bank money managers, such as MMFs. In doing so, the Fed signaled the critical status of the MMF industry. The Fed also crafted its policies to strengthen the balance sheet of these funds. For example, Fed lifted limits on the amount of financial cash the companies could park at the central bank from $30bn to $80bn. The absence of profitable investments has compelled MMFs to use this opportunity and place more assets with the reverse repurchase program. The goal was to drain liquidity from the system, slow down the downward pressure on the short-term rates, and improve the industry’s profit margin. The Fed’s balance sheet access drove the MMFs to a higher layer of the monetary hierarchy.

The Fed might have improved the position of the MMFs in the monetary hierarchy. However, it could not expand the ability of the MMFs to invest the money fast enough. The mismatch between the size of the MMFs and the amount of liquidity in circulation created balance sheet problems for the industry. On the liabilities side, the money under management has increased dramatically as the large-scale economic stimulus from the Fed and the US government created excess demand for short-dated Treasuries and other securities. Therefore, assets in so-called government MMFs, whose investments are limited to Treasuries, jumped above $4tn for the first time. But, on the asset side, it was a shortage of profitable investments. The issue was that too much money was chasing short-term debt, just as the US Treasury started to scale back its issuance of such bills. This combination created downward pressure on the rates. The industry was not large enough to service a large amount of cash in the system.

The downward pressure on rates was intensified despite the Fed’s effort to include the MMFs in the reserve repurchase (RRP) facility. The dearth of suitable investments has compelled MMFs to place more assets with an overnight Fed facility. Yet, as the RRP facility paid no interest, it could not resolve a fundamental threat to the economics of the MMF industry, the lack of profitable investment opportunities. Once the post-pandemic monetary policy stance made the economics of the MMF industry alarmingly unsustainable, the Fed chose to start the normalization process and increase the RRP rates. The point to emphasize is that the timing of the Fed’s monetary policy normalization matches the developments in the MMF industry rather than banks.

This shift in the Fed’s focus away from the banks and towards the MMFs yields mixed results for the banks, although it is unequivocally helping MMFs. First, the increase in RRP has strengthened the asset side of MMFs’ balance sheets as the policy has created a positive-yielding place to invest their enormous money under management. Second, other normalization policies, such as the rise in the federal funds rate and interest on excess reserve (IOER), are increasing rates, especially on the short-term assets, such as repo instruments. This adjustment has been critical for the smooth functioning of the MMFs as the repo rate was another staple source of income for the industry. Repo rate, the rate at which investors swap Treasuries and other high-quality collateral for cash in the repo market, had also turned negative at times. Overall, the policies that supported MMFs also improved the state of the short-term funding as the MMF industry plays a crucial role in the market for short-term funding.

The Fed policies are creating problems for the liabilities side of specific types of banks, bond-heavy banks. As Zoltan Pozsar noted, the Fed’s recent move to stimulate the economy through the RRP rate hurts banks’ liabilities. Such policies encourage large corporate clients to direct cash into MMFs. The recently generated outflow following the normalization process is being forced on both cash-rich and bond-heavy banks. This outflow is in addition to the trend above, where cash-rich banks have deliberately pushed the deposits outside their balance sheets and orchestrated the “run on their own banks.” The critical point is that while cash-rich banks’ business model encourages such outflows, they will create balance sheet crises for the bond-heavy banks, which rely on these deposits to finance their long-term securities. The Fed recognizes that bond-heavy banks can not handle the outflows. Still, the non-bank financial intermediaries have become the center of the Fed’s policies as the main financiers of the real economy.

The Fed is relying on non-bank intermediaries rather than banks for monetary normalization. To this end, the Fed has modified its FRB/US model to capture MMFs as the source of credit creation. The new signals evolve within the new monetary framework are suggesting that new identification is here to stay. First, the financial market echoed and rewarded the Fed after making such adjustments to assume financial intermediation. The market for short-term funding was reset shortly after the Fed’s announcements. The corrections in the capital market, both in stocks and bonds, were smooth as well. Second, after all, the Fed’s transition to primarily monitor MMFs balance sheet is less of a forward-looking act and more of an adjustment to a pre-existing condition. Researchers and global market-watchers are reaching a consensus that non-bank financial intermediaries are becoming the de-facto money lenders of the first resort to the real economy. Therefore, it is not accidental that the policy that restored the short-term funding market was the one that directly supported the MMFs rather than banks. Here’s a piece of good news for the Fed. Although the Fed’s traditional, bank-centric, “policy” tools, including fed funds target, are losing their grip on the market, its new, non-bank-centric “technical” tools, such as RRP, are able to restore the Fed’s control and credibility.

Elham Saeidinezhad is lecturer in Economics at UCLA. Before joining the Economics Department at UCLA, she was a research economist in International Finance and Macroeconomics research group at Milken Institute, Santa Monica, where she investigated the post-crisis structural changes in the capital market as a result of macroprudential regulations. Before that, she was a postdoctoral fellow at INET, working closely with Prof. Perry Mehrling and studying his “Money View”. Elham obtained her Ph.D. from the University of Sheffield, UK, in empirical Macroeconomics in 2013. You may contact Elham via the Young Scholars Directory